Netflix: The Market Got There First

July 15, 2026 | Five firms cut their average Netflix target 18% in a month. Every new target still sits above the stock—and Thursday’s consensus never moved.

Verdict: ahead of Wall Street, not yet proven right.

1–3 months: Thursday tests whether the market moved too far.

12+ months: Churn, engagement and advertising decide whether the analysts’ remaining upside survives.

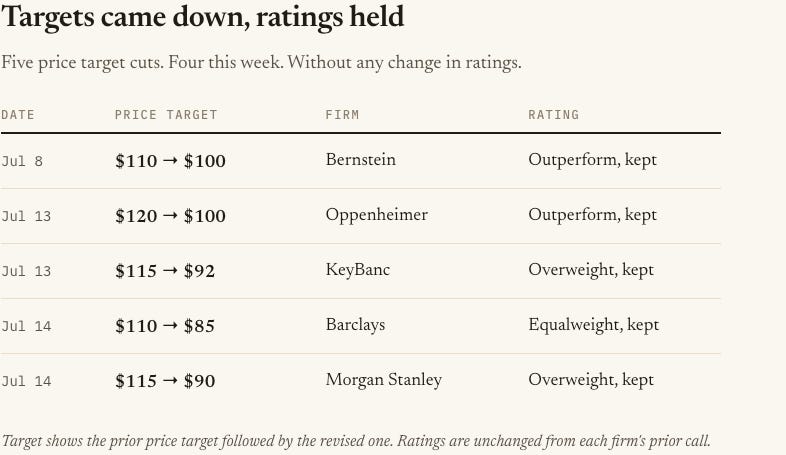

Five target cuts. Four this week.

That is Netflix going into Thursday’s second-quarter report:

Each action is linked to published coverage of the firm’s note. Netflix closed Tuesday at $73.53, down about 2% on the day.

Before the cuts, those five targets averaged $114. They now average $93.40. That is an 18% markdown from the same five firms, with most of it arriving over Monday and Tuesday.

The market got there first

Barclays is the least optimistic desk in the table. Its new $85 target is still 16% above Tuesday’s close. Morgan Stanley’s $90 implies 22% upside. All five firms cut what they think Netflix is worth and still landed above the market.

The broader tape leans the same way: 37 buys, 13 holds and no sells among the 50 analysts in the dataset I use. The ratings and targets agree. The market disagrees with both.

That does not make the market wrong. It makes Thursday a test of whether the stock’s harsher markdown was foresight or overshoot. Wall Street lowered its estimates. Investors had already lowered the price further.

The quarter refused to join the downgrade

Here is the more interesting split: the consensus for Thursday did not move. Analysts still expect roughly $12.57 billion in revenue and $0.79 in earnings. The $0.79 estimate has been unchanged for a month.

KeyBanc shows the anatomy of the cut. Justin Patterson lowered his target 20% while expecting a largely in-line quarter. He trimmed 2026 earnings by 1%, 2027 earnings by 4%, and applied a lower valuation multiple.

Same quarter. Less faith in the years after it.

That distinction matters on Thursday. Netflix can beat an unchanged quarterly estimate and still fall if guidance, engagement or the longer-term earnings path disappoints. “Beat” and “good report” are not synonyms when the argument has moved beyond the quarter.

Five cuts, several arguments

KeyBanc pointed directly to engagement concerns weighing on valuation. Morgan Stanley reached the same target-cut decision from a different premise: credit-card data showed a larger-than-usual churn spike after price increases. But Sean Diffley called engagement worries “largely overblown” and expects the second-half live-events and sports slate to help.

Bernstein cut near-term subscriber estimates and lowered the multiple it applies to earnings. Public coverage of the Barclays and Oppenheimer notes confirms their cuts, but not a rationale. Five firms cut. They did not all make the same argument.

The engagement concern still has evidence behind it. Digital i, using opt-in panels across 20 international markets, found daily Netflix viewing per account fell from 100.5 minutes in 2024 to 93.4 in 2025. YouTube rose to 99.1.

Netflix offers a different scoreboard. Its April shareholder letter said its primary internal quality engagement metric reached an all-time high.

Both can be true because they measure different things. Digital i counts minutes per account in a panel. Netflix has not disclosed how its quality metric is built. One measures quantity; the other asks readers to trust an undisclosed definition of quality. That does not make Netflix wrong. It does leave the dispute open.

Cheap against the past, not necessarily the future

Netflix is down about 22% this year and 42% from its 52-week high. At roughly 26 times free cash flow, it sits at the bottom of its own two-year valuation range.

That is real cheapness against history. It is not proof that the history still deserves to be the benchmark. The valuation comparison looks backward; the target cuts are about growth and valuation ahead. A rear-view mirror can tell you how far the price has traveled. It cannot tell you whether the road changed.

What Thursday can actually settle

The first score is $12.57 billion and $0.79. The more important scores may arrive in guidance, churn commentary and whatever Netflix chooses to disclose about engagement.

Netflix has sold off the day after each of its last four reports—5.1%, 10.1%, 2.2% and 9.7%. Four observations are a warning, not a law of physics. They are enough to treat any first green headline as an opening reaction, not a verdict.

The report can also move the longer-term argument without settling it. Netflix has said content-amortization growth is weighted to the first half of 2026, so a softer Q2 margin alone does not break its 31.5% full-year target. Its half-year engagement report is expected with the release, but that report lists hours viewed by title. It does not answer the per-account question raised by Digital i.

My read

Three things matter after the numbers cross:

A beat is the first answer, not the last one. The quarterly consensus stayed put while the forward view came down. A better-than-expected quarter paired with soft guidance can still sell off because the argument moved beyond EPS.

The overshoot case needs three things. Firm guidance, evidence that post-price-hike churn is normalizing, and engagement data readers can compare with the outside evidence. A close back above the low $80s would be the first genuine chart repair since April.

The market-ahead case has a line. $70.86 is the 52-week low. Weak guidance or persistent churn followed by a break below it would say the analysts still have catching up to do.

Analysts edit spreadsheets more readily than adjectives. When targets fall but ratings stay put, ignore the label and ask three questions: Did the quarterly consensus move? Did longer-term estimates or valuation change? Did the price move further than both? Here the answers are no, yes and yes. That puts the risk in guidance and the call, not just the EPS headline. The numbers usually confess first.

Disclaimer: This is not The Hunger Games, although the odds may still refuse to cooperate and the sponsors are nowhere to be found. This is research, not financial advice or a recommendation. Check the evidence, understand your risk, and make your own decision before entering the arena.